Practical Tips Concerning House Mortgages That Easy To Follow

Authored by-Burke WeissA mortgage is truly a huge milestone in a person's life, whether they are 18 or 80 when they get it. The fact is that knowing the right things before you get started can make the process better. This article has what you need to know, so read it in full.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

Save enough money to make a down payment. Lenders may accept as little as 3.5% down but try to make a larger down payment. If you put down 20% of your total mortgage, you won't have to pay private mortgage insurance and your payments will be lower. You will also need cash to pay closing costs, application fees and other expenses.

If the idea of a mortgage looming over your head for the next few decades does not appeal to you, consider refinancing over a shorter period. Although your monthly payments will be more, you'll save a lot in terms of interest over the life of the loan. It also means being mortgage-free much sooner, and owning your home outright!

You probably need a down payment. In years gone by, some lenders didn't ask for down payments, but those days are mostly over. You should ask how much you will have to spend on your down payment before submitting your application.

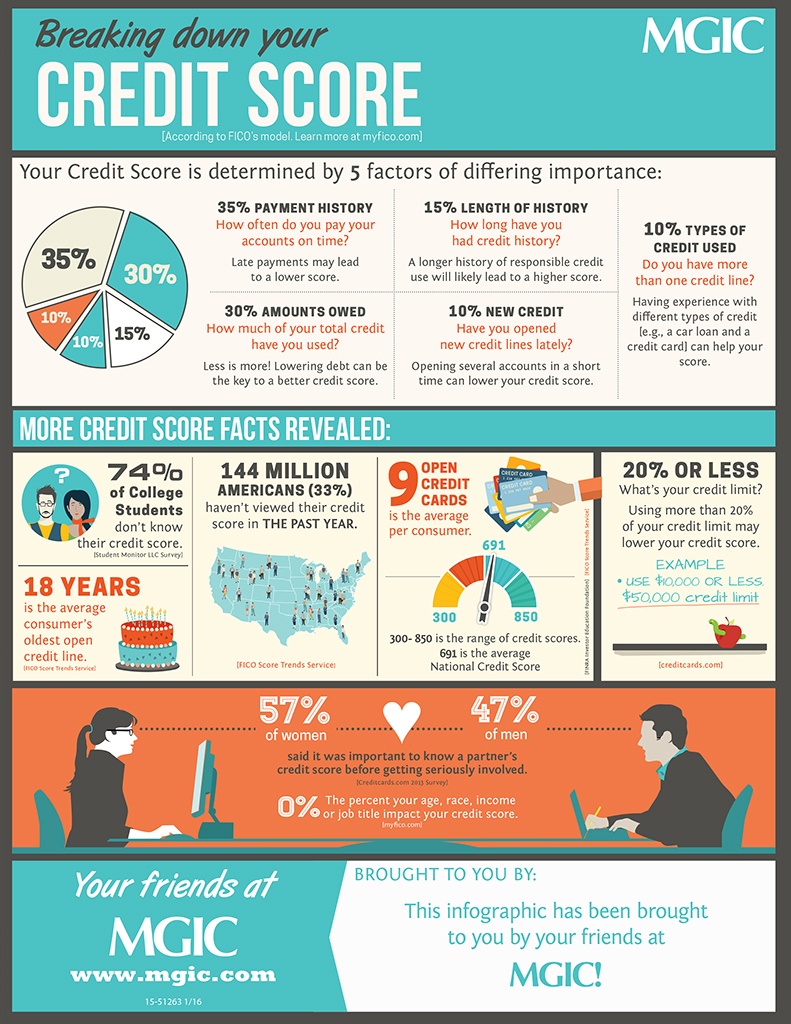

Know your credit score before going in to get a mortgage. Your potential lender will do their own homework on this, but you should arm yourself with the intel as well. Knowledge is power in terms of the negotiations to follow. If you aren't clear on your strengths and weaknesses, then a lender can more easily use the knowledge against you.

Locate the lowest rate for interest you can find. simply click the up coming website is seeking the best way to get you locked in at an interest rate that is high. Avoid being the next person they sucker in. Give yourself several choices by looking at many offers from different lenders.

Consider having an escrow account tied to your loan. By including your property taxes and homeowners insurance into your loan, you can avoid large lump sum payments yearly. Including these two items in your mortgage will slightly raise the monthly payment; however, most people can afford this more than making a yearly tax and insurance payment.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

There are many different types of home mortgage loans available, and some are much easier to get than others. If you are having a problem getting a conventional loan, try applying for an adjustable rate mortgage or a balloon. These are short term loans ranging from one to 10 years, and need to be converted when they expire.

Know https://timesofindia.indiatimes.com/business/india-business/fintech-banking-to-help-serve-every-indian/articleshow/82377410.cms that goes into the mortgage and what you are getting fee wise so that you know what's going to happen. Closing costs and other fees should be itemized. It's possible that you may be able to negotiate these fees with either the lender or the seller.

Take the time to get your credit into the best shape possible before you look into getting a home mortgage. The better the shape of your credit rating, the lower your interest rate will be. This will mean paying thousands less over the term of your mortgage contract, which will be worth the wait.

Do not change financial institutions or move any money while you are in the process of getting a loan approved. If there are large deposits and/or money is being moved around a lot, the lender will have a lot of questions about that. If you don't have a solid reason for it, you may end up getting your loan denied.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

If you have credit issues or none at all, the only way to get qualified for a home mortgage loan is through alternative sources. Keep records of all your payments for the last year. Proving a steady record of paying utilities and rent is good for borrowers who have poor credit.

Investigate preapprovals before you start home shopping. Preapproved mortgages will give you an idea of both how much home you can afford plus what your monthly mortgage payments will be. This will set the parameters of your home shopping and save you time not looking at properties you can't realistically afford.

One item of documentation for home mortgage application that is often overlooked is a gift letter. If your relatives have chipped in to help you make your down payment, you may need to document your source of income. This really depends on the type of home mortgage you get. Some require this, and others do not. Play it safe by getting a gift letter from anyone who gives you money to help you buy your home. Have this on file with your other documentation.

Look into credit unions. There are many options for obtaining financing and credit unions have their strengths. Often credit unions will hold mortgages in their private portfolio. Banks and other financial institutions routinely sell mortgages to other holding companies. This could result in your loan changing hands multiple times over its lifetime.

You now see how being educated on home mortgages can lessen your stress when searching for that perfect place to live. It does not have to be that hard, and in fact it is a simple process when you have wise information such as the tips that were presented here. Read them again if you have to, and be confident the next time you apply for a home mortgage.